Systematic Investment Plans (SIPs) are one of the most popular ways to invest in mutual funds in India. They allow investors to invest a fixed amount regularly and build wealth over time.

However, many beginners unknowingly make SIP mistakes that can reduce their returns significantly.

A SIP works best when investors follow a disciplined long-term strategy. But mistakes like stopping SIPs during market crashes, choosing the wrong funds, or investing without a goal can damage your portfolio.

In this guide, we’ll discuss 7 common SIP mistakes that can kill your returns and how you can avoid them to make the most of your investments.

Table of Contents

What is SIP Investing?

A Systematic Investment Plan (SIP) is a method of investing in mutual funds where you invest a fixed amount regularly (monthly, weekly, or quarterly).

Instead of investing a large lump sum, SIP allows you to invest small amounts consistently.

For example:

| Month | SIP Amount | NAV | Units Purchased |

|---|---|---|---|

| Jan | ₹2000 | ₹20 | 100 units |

| Feb | ₹2000 | ₹18 | 111 units |

| Mar | ₹2000 | ₹22 | 90 units |

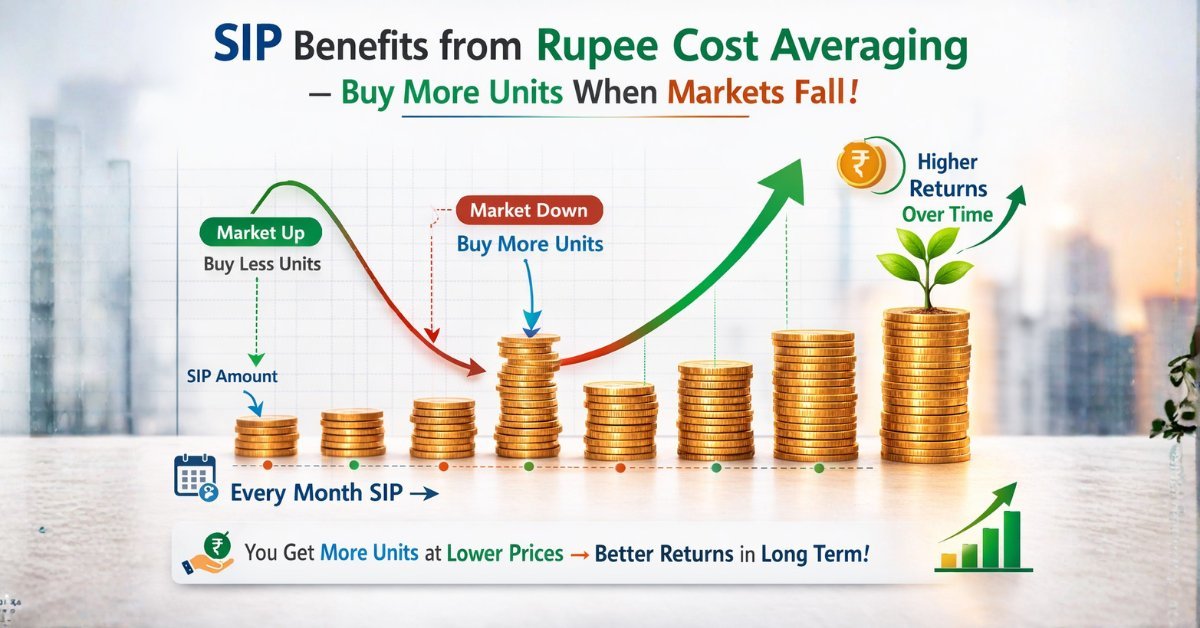

Over time, SIP benefits from rupee cost averaging and compounding.

If you’re new to mutual funds, you can also read our guide on what is a mutual fund to understand how these investments work.

Why Avoiding SIP Mistakes is Important

Many investors think that simply starting a SIP guarantees good returns. But the reality is different.

Poor decisions and emotional investing can reduce the benefits of SIP.

Avoiding SIP mistakes helps you:

- maximize long-term returns

- build disciplined investing habits

- reduce investment risks

- stay focused on financial goals

Avoid these SIP mistakes:

SIP investing is simple, but even small mistakes can significantly reduce your long-term returns. Many beginners stop their SIPs during market crashes, choose mutual funds without research, or invest without clear financial goals. These SIP mistakes often happen due to lack of knowledge or emotional decisions during market volatility.

To build wealth successfully through SIPs, investors should focus on long-term discipline, proper fund selection, and regular portfolio reviews. Staying invested consistently and increasing SIP amounts as income grows can help maximize the benefits of compounding. By avoiding these common SIP mistakes, you can create a stronger investment strategy and achieve your financial goals more effectively.

Common SIP Mistakes That Can Kill Your Returns

1. Stopping SIPs During Market Crashes

One of the biggest SIP mistakes is stopping investments when markets fall.

Many investors panic during market corrections and pause their SIPs.

But market downturns actually help SIP investors.

When markets fall:

- NAV becomes lower

- SIP buys more units

- long-term returns improve

Example:

If the NAV drops from ₹20 to ₹15, your SIP buys more units for the same investment.

This improves your average cost over time.

2. Investing Without a Clear Goal

Another common SIP mistake is investing without a financial goal.

Many beginners start SIPs randomly without knowing why they are investing.

A SIP should always be linked to goals like:

- retirement

- children’s education

- buying a house

- building long-term wealth

When you invest with clear goals, you can:

- choose the right mutual funds

- decide the correct investment period

- stay disciplined during market volatility

3. Choosing Funds Without Proper Research

Not all mutual funds are suitable for SIP investing.

Many investors choose funds based on:

- recent high returns

- tips from friends

- social media recommendations

This is risky.

Instead, you should analyze:

- fund category

- historical performance

- fund manager experience

- expense ratio

- risk level

The Association of Mutual Funds in India (AMFI) provides reliable information about mutual fund schemes and regulations.

You can learn more from the official AMFI website.

4. Not Increasing SIP Amount Over Time

Many investors start a SIP and continue with the same amount for years.

But as income increases, SIP investments should also increase.

This strategy is called Step-Up SIP.

Example:

| Year | Monthly SIP |

|---|---|

| Year 1 | ₹3000 |

| Year 2 | ₹4000 |

| Year 3 | ₹5000 |

Even a 10% increase every year can significantly boost long-term wealth.

5. Investing for Too Short a Period

SIP is designed for long-term investing.

Many beginners stop SIPs within 1–2 years if returns are not high.

But equity mutual funds need time to perform.

Recommended SIP duration:

| Investment Type | Ideal Duration |

|---|---|

| Equity Funds | 5–10 years |

| Hybrid Funds | 3–5 years |

| Debt Funds | 2–3 years |

Long-term investing allows compounding to work effectively.

You can understand this better by learning about the power of compounding in mutual funds.

6. Trying to Time the Market

Another common SIP mistake is trying to predict market movements.

Some investors stop SIPs when markets rise and restart them during corrections.

But market timing rarely works consistently.

SIP works best when you:

- invest regularly

- ignore short-term volatility

- focus on long-term growth

Even professional investors struggle to time the market correctly.

7. Ignoring Portfolio Reviews

Many investors start SIPs and never review their investments.

This can lead to problems like:

- underperforming funds

- high-risk portfolios

- outdated investment strategies

Ideally, review your SIP portfolio once or twice a year.

You can check:

- fund performance

- asset allocation

- goal progress

The Securities and Exchange Board of India (SEBI) also encourages investors to stay informed about their investments and review portfolios regularly.

Beginner Tips for SIP Investors

If you want to avoid SIP mistakes, follow these practical tips:

Start Early

The earlier you start investing, the more you benefit from compounding.

Stay Consistent

Do not stop SIPs during market volatility.

Diversify Investments

Invest across different mutual fund categories.

Increase SIP Over Time

Increase SIP amount whenever your income increases.

Choose Funds Carefully

Always research funds before investing.

FAQs

1. What is the biggest SIP mistake beginners make?

The biggest SIP mistake is stopping SIPs during market downturns. Market corrections actually help SIP investors buy more units at lower prices.

2. Can SIP give negative returns?

Yes, SIP investments in equity funds can give negative returns in the short term. However, long-term investing usually reduces this risk.

3. How long should I continue a SIP?

For equity mutual funds, SIP investments should ideally continue for at least 5–10 years to benefit from compounding.

4. Should I stop SIP when the market is high?

No. SIP works best when investments continue consistently regardless of market conditions.

5. Is SIP better than lump sum investment?

Both methods have advantages. SIP is better for disciplined investing and risk reduction. You can read our detailed comparison in SIP vs Lump Sum – Which is Better?

Can I pause SIP temporarily?

Yes, most mutual funds allow investors to pause SIP temporarily. However, frequent pauses may reduce the long-term benefits of disciplined investing.

Conclusion

SIP is one of the easiest and most effective ways to build long-term wealth.

But avoiding common SIP mistakes is essential to maximize your returns.

Remember these key lessons:

- stay invested during market crashes

- invest with clear financial goals

- choose funds carefully

- increase SIP amount over time

- review your portfolio regularly

With discipline and patience, SIP investing can help you achieve your financial goals.

Continue Learning

If you’re new to investing, also read our guide on What is SIP? Meaning, Benefits, and How SIP Works to understand the basics of systematic investment plans.

Jitendra Bhandari is the founder of PaisaBhi, a personal finance platform that explains investing, mutual funds, and money management in simple language for beginners in India.

Financial Disclaimer

The information provided on PaisaBhi.com is for educational and informational purposes only and should not be considered financial advice. Investments in mutual funds and the stock market are subject to market risks. Please consult a certified financial advisor before making any investment decisions. Read all scheme-related documents carefully before investing.